Startups in the sector have raised over $1.28 billion since 2019. A third of the capital now comes as debt, in larger rounds, and from lenders rather than venture investors, a sign the sector is being financed like infrastructure

For most of the last decade, investing in an African electric mobility startup was a bet on an unproven market. Our latest analysis of the funding data says that era is closing. Companies building electric two- and three-wheelers, e-buses, battery-swap networks and the financing to put vehicles under riders have raised $1.28 billion across 129 deals between 2019 and early June 2026, according to the TechCabal Insights Deal Tracker. The African Development Bank (AfDB) sees the same shift. According to Wale Shonibare, the director energy financial solutions, policy and regulation:

“The Bank’s approach to supporting e-mobility operators is evolving and financing is now contingent on three conditions: scalable, commercially viable business models, predictable revenue streams, and an enabling regulatory environment. To back that transition, AfDB is developing the Green Mobility Facility for Africa (GMFA), a blended finance platform expected to mobilize more than $300 million to unlock commercial lending, support pipeline development and deploy capital through a mix of instruments including guarantees and financial intermediation with commercial banks.”

Debt now funds a third of the sector, capital is arriving in larger rounds, and the companies winning it are increasingly looking like infrastructure operators.

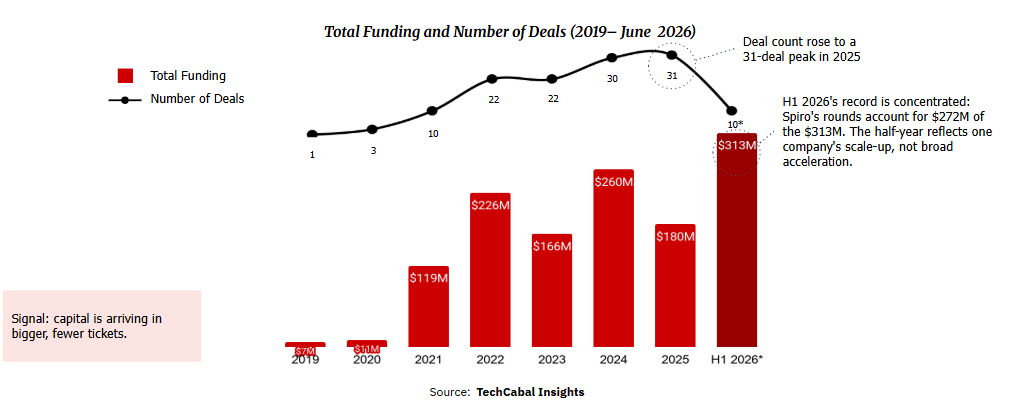

The climb has not been steady. Annual funding swung from $119 million in 2021 to $260 million in 2024, dipped to $180 million in 2025, then jumped again. In the first half of 2026 alone, the sector raised $313 million, more than all of 2025, on just ten deals. That record carries a caveat worth stating plainly: Spiro, the electric two-wheeler and battery-swap company, accounts for about $272 million of it, so the half-year reflects one company’s scale-up rather than a broad acceleration.

Deal activity rose every year through 2025, and since 2021, rounds of $10 million or more have taken at least three-quarters of annual funding. The market now funds build-out, not just experiments.

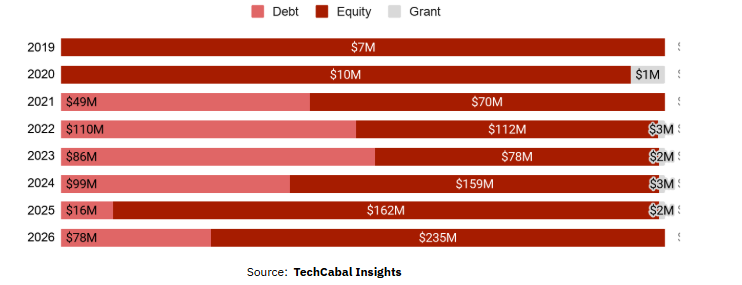

Share of Total Funding by Type (2019– June 2026*)

Debt is the signal

The clearest signal sits in the kind of capital. Equity still leads at 65% of the total, but debt has climbed to 34% ($437 million), from nothing in 2019, and it overtook equity in 2023. Lenders enter a sector only once its assets can be collateralised and its receivables predicted.

“Mobility financing businesses are debt-intensive by nature,” says Dieko Ojo, an investment associate at Novastar Ventures, “and the ability to scale depends heavily on access to affordable and appropriately structured debt.”

She points to the constraint that shapes the whole market: these businesses need patient capital, and when debt is expensive, too much operating cash goes to servicing it, slowing how fast operators can reach riders.

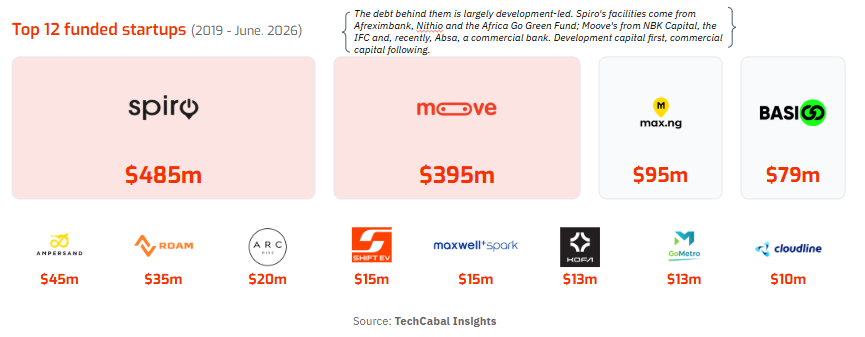

That debt is largely development-led, from institutions such as Afreximbank and the International Finance Corporation (IFC) and climate-focused funds, with commercial banks like Absa only beginning to follow. It funds physical, revenue-generating assets: fleets, batteries and swap stations. Spiro frames the logic directly, calling electric mobility and energy infrastructure two sides of the same coin and positioning itself as an energy platform rather than an EV maker, with more than 2,500 swap stations deployed. The proof that this can pay is recent.

“We are already cash positive in our two most mature markets,” the company told TechCabal Insights, the kind of cash generation that defines infrastructure, not venture.

Capital clusters around a proven few

The market’s other defining feature is its narrowness. Four companies hold 82% of all capital, and the top twelve hold 95%, a power-law distribution in which Spiro ($485 million) and Moove ($395 million) alone command 69%. Nigeria and Benin account for 77% of funding, but strip out Moove and Nigeria falls to $104 million, and strip out Spiro and Benin practically disappears. The breadth sits in Kenya, where 39 deals worth $143 million make East Africa the sector’s experimentation base.

For riders, it is an economics story

For the people the sector serves, the daily economics are the point. Going electric cuts a rider’s biggest running cost. Ampersand, the Rwandan e-motorcycle company, says its bikes cost half as much to power as petrol ones, which by its numbers saves riders around $700 a year and lifts take-home pay by about 45%, while financing models such as Moove’s use alternative credit scoring to bring drivers into vehicle ownership and formal credit, often for the first time.

Policy is catching up: more than half of 21 African countries assessed by the United Nations Environment Programme (UNEP) and Africa E-mobility Alliance (AfEMA) have set e-mobility targets and incentives, driven largely by the cost of fuel imports.

The AfDB director’s assessment reinforces the point:

“Countries that have introduced targeted incentives, such as fiscal exemptions, supportive tariffs and clear EV standards, are already seeing stronger pipelines and investor interest, with Kenya, Rwanda and Ethiopia leading. The Bank is channelling capital accordingly, backing equity and debt funds including Persistent Africa Climate Venture Builder Fund, Zafiri and FEI across markets with strong policy momentum”.

The funding data shows a sector that has begun to attract infrastructure-style capital, not just venture bets. But that shift is narrow. Two companies hold 69% of all capital and 78% of the debt, and only 51 startups have raised at all, so the asset-class case still rests on a handful of bellwethers proving the model. The largest opening sits where the demand is, in commercial two- and three-wheelers, the income-generating fleet that moves most of urban Africa.